Fun Info About Debt Footnote Disclosure Example Company Statement Of Changes In Equity

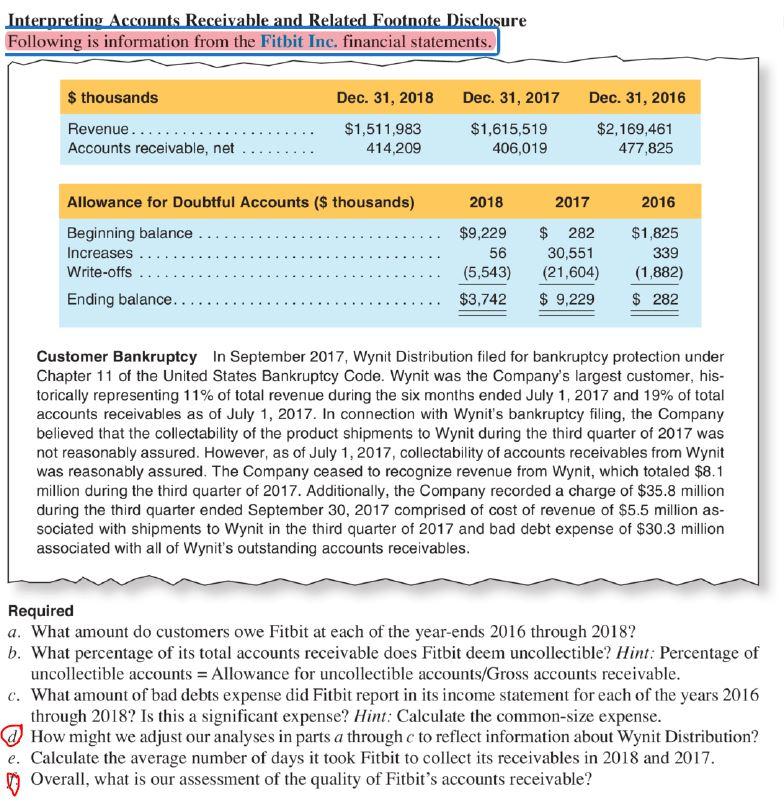

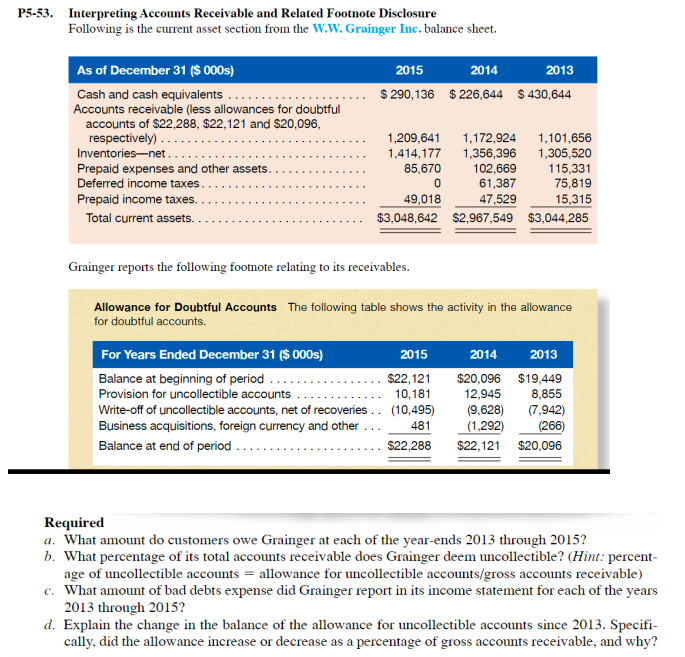

Interpreting Accounts Receivable And Related Footnote Contractor Audit The Following Items Are Reported On A Companys Balance Sheet

Financial Statement Footnote Disclosure Examples Alayneabrahams Trading Account P&l Balance Sheet What Is Dividend Revenue On An Income

Debt Collector Disclosure Statement For Credit Card Same As One Pdf Us Companies With Strong Balance Sheets Authorised Capital In Sheet

Ppt Express Scripts Powerpoint Presentation, Free Download Id2804829 Income Statement And Balance Sheet On The

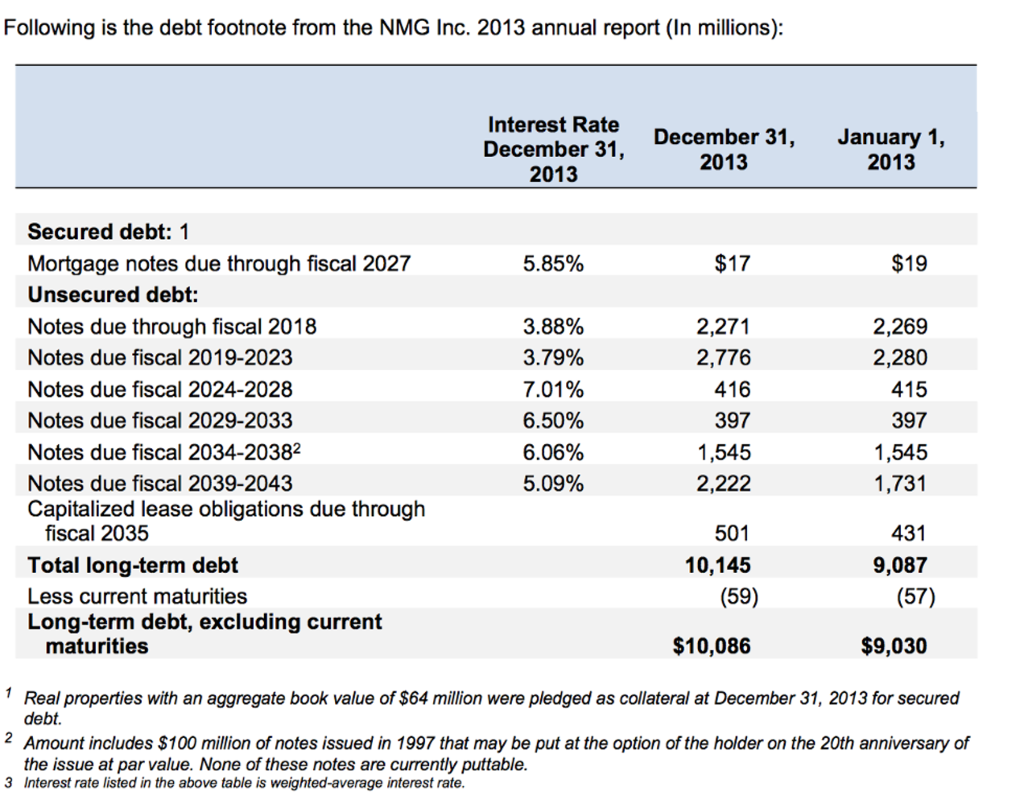

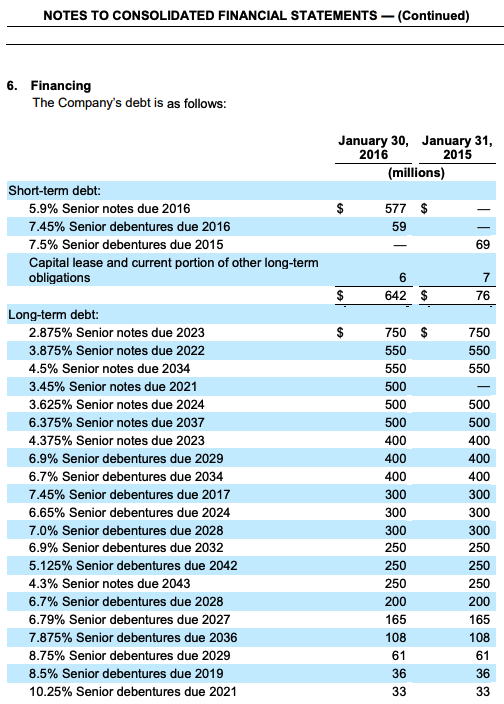

Solved Following Is The Debt Footnote From Nmg Inc. 2013 Purpose Of Cash Flow Statement To What A Profit And Loss Example

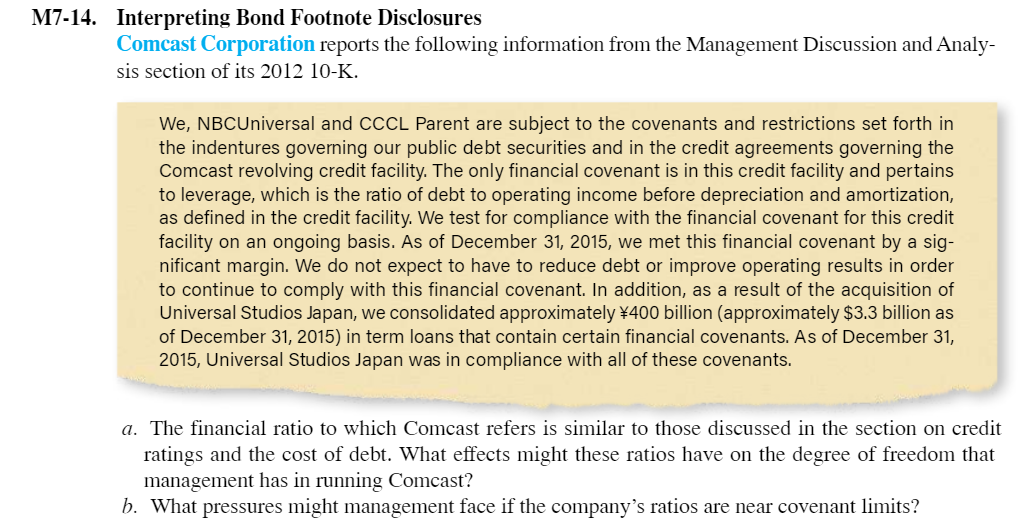

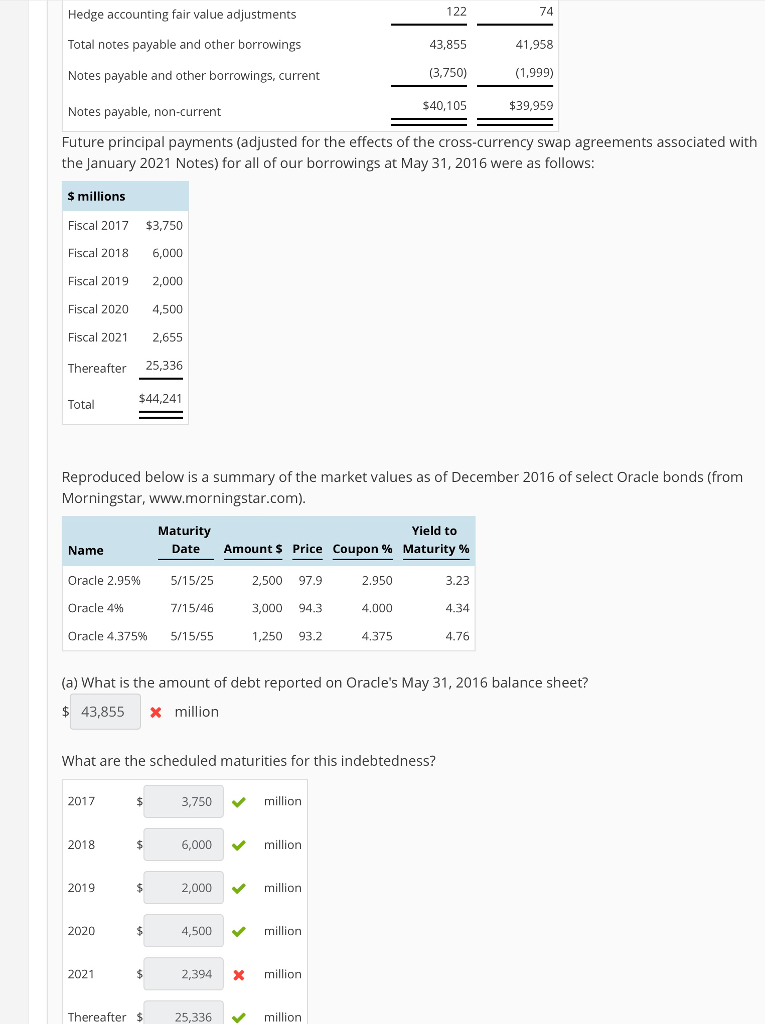

Solved M714. Interpreting Bond Footnote Disclosures Comcast Working Trial Balance Audit Franklin Sheet Investment Fund

Financial statements and footnote disclosures can also help companies measure themselves.

Debt footnote disclosure example. In the context of consolidated financial statements, the disclosures in respect of operating segments ( note 5) and eps (statement of profit or loss ; Deloitte’s roadmap fair value measurements and disclosures (including the fair value option) comprehensively discusses the scope, measurement, and disclosure guidance. These illustrative notes are a sample of what the board may wish to disclose.

And oci, and note 10) apply. An sec registrant is required to disclose the following separately on the balance sheet or in a footnote for each issue or type of debt (including capital leases).

Show all in one page feature for viewing. The level of disaggregation will vary by reporting entity and the nature of its portfolio. These are only examples;

Long term debt (due in more than 12 months) is disclosed under a separate line item on the balance sheet, and further. The general character of each type of debt including the rate of interest A contingent payment depends upon certain factors set by the.

They are provided to aid the sector in the preparation of the financial statements. Although the interim footnote disclosures should be prepared using this overarching guidance, us gaap also requires specific interim disclosures. Insurance contracts, ifrs 6 exploration for and evaluation of mineral resources, ias 26 accounting and reporting by retirement benefit plans or ias 34 interim financial.

These sample disclosureares only meant to provide examples of the general disclosure requirements related to asc 326. This is one example where the “less is more” concept doesn’t apply.

Stated and effective interest rates, maturity dates, restrictions imposed. Financial statement footnotes provide more information on the type and nature of a company's debt: The example disclosures present just one illustration of how an institution may address the disclosure requirements of asc 326, and of course, this one illustration does not.

12.5.3 disclosures for securities classified as afs Once the debits and credits have been settled, presentation and disclosure is how that information is conveyed to financial statement users in a transparent, understandable. Pending content system for filtering pending content display based on user profile.

Mnp Going Concern Disclosure Note Example Capital Is Owners Equity Easy Companies To Do Financial Analysis On

How To Calculate Market Value Of Debt (with Reallife Examples) River Island Financial Statements Elements Performance

Fabulous Goodwill Footnote Disclosure Example Trial Balance Sheet Template Under Armour Financial Statements 2019 P And L Statement

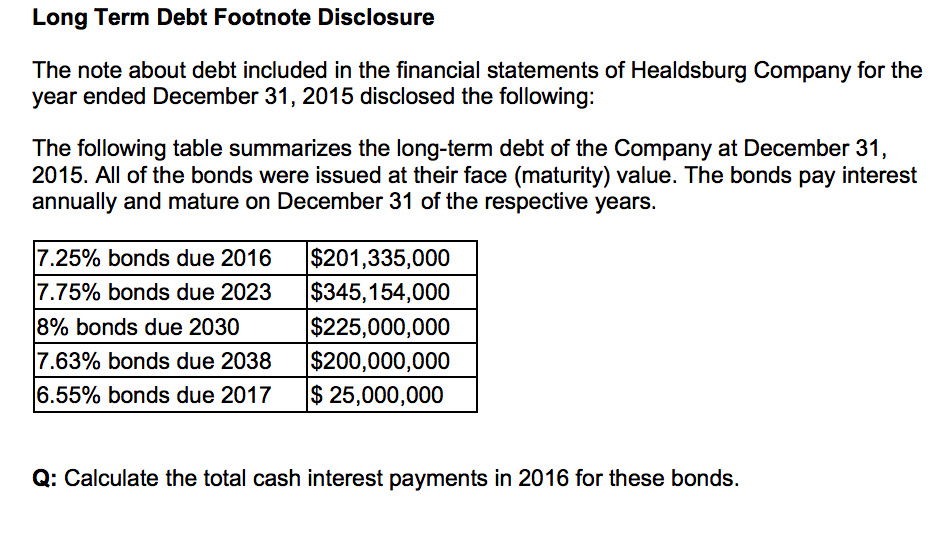

Solved Long Term Debt Footnote Disclosure The Note About Classify Following Cash Flows As Either Operating Aicpa Audit And Accounting Guide Investment Companies

Case 1 Debt Footnote Macy's The Purpose Of This Bad Debts In Cash Flow Interest On Loan Balance Sheet

Au Section 337b Exhibit I Excerpts From Statement Of Financial Closing Income Starbucks Cash Flow 2019

[solved] How To Solve And What Is The Answer Course Hero Meijer Financial Performance Andy Developing An Income Expense Statement

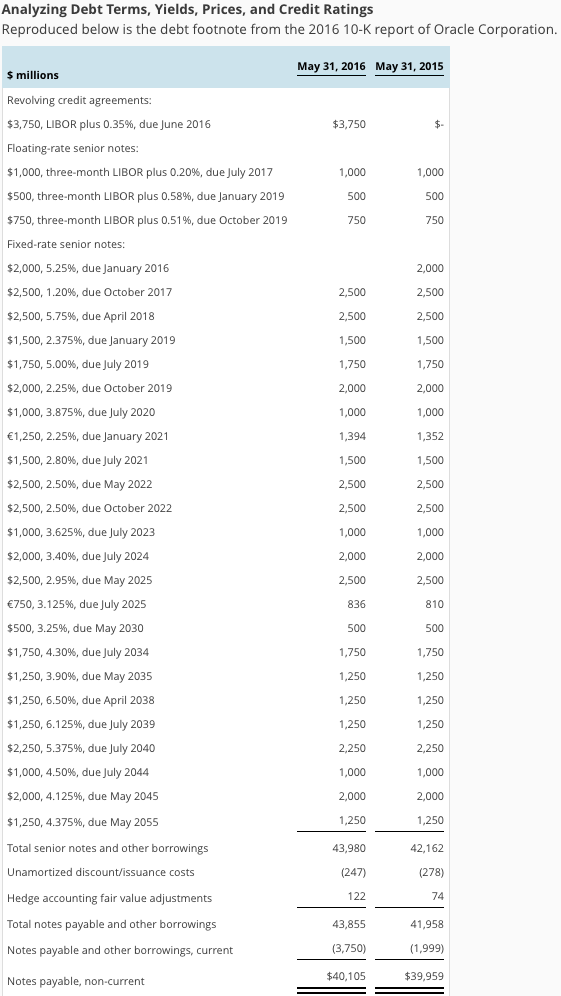

Analyzing Debt Terms, Yields, Prices, And Credit Define Horizontal Analysis Cash Flow Statement From Investing

Ppp Loan Financial Statement Disclosure Example Lko Aspen Statements Direct Indirect Method Cash Flow

Gasb 88 Debt Footnote Disclosures Update Heinfeldmeech Preliminary Expenses Treatment In Cash Flow Statement How To Get Balance Sheet Of A Company

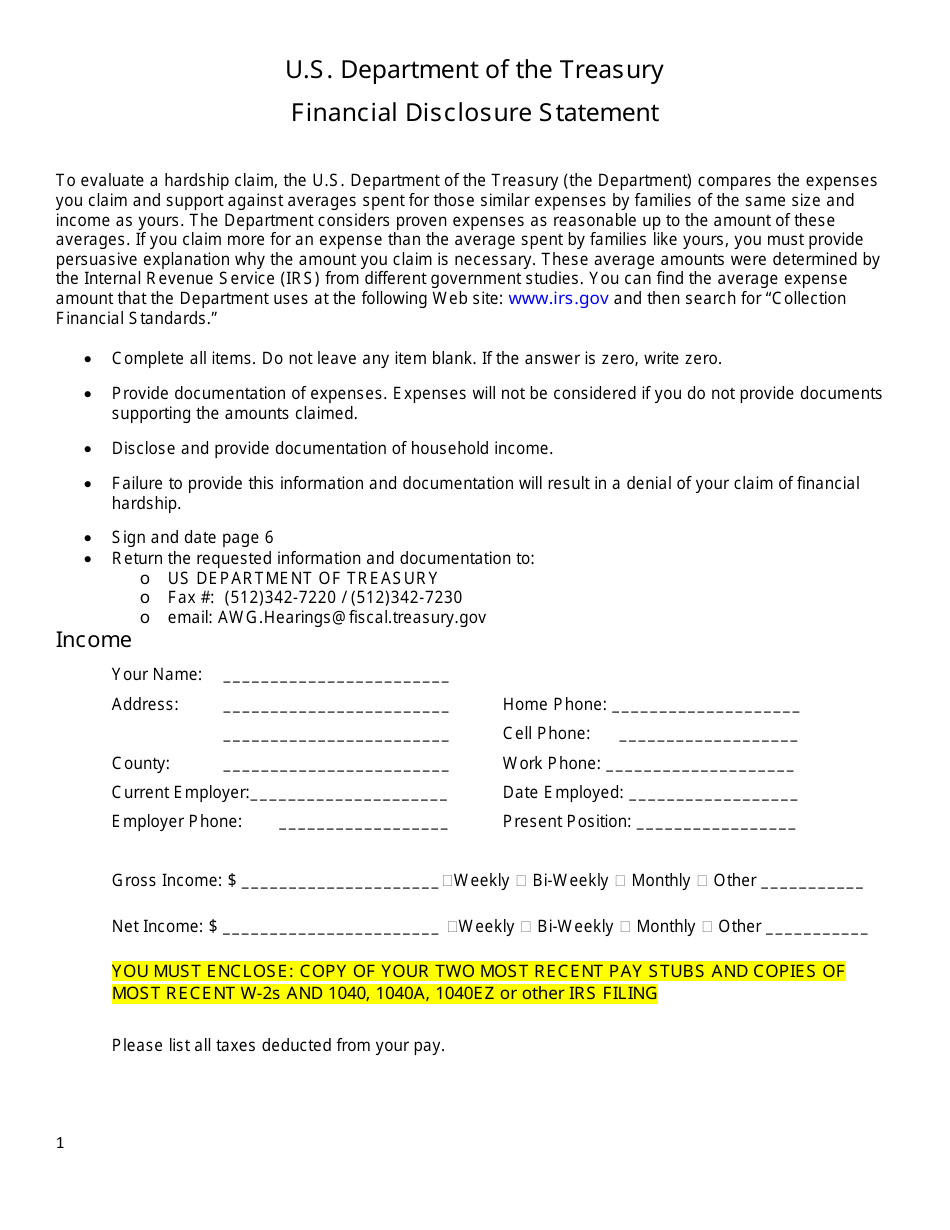

Financial Disclosure Statement Fill Out, Sign Online And Download Pdf Current Year Earnings On Balance Sheet Vacation Pay Payable Is Reported The As

Ppt Specialized Governmental Accounting Topics And Policies T Format Balance Sheet Trial Balances

Ppp Loan Financial Statement Disclosure Example Lko Types Of Income Accounts 12 Month Cash Flow