Recommendation Tips About Reporting Comprehensive Income Panera Bread Financial Statements

(pdf) The Method Of Choice For Reporting Comprehensive Cash And Equivalents In Balance Sheet Basic Financial Statement Template

Comprehensive Credit Reporting Cpd Rise Making A Balance Sheet Ethiopian Airlines Financial Statements

Ppt Retained Earnings, Treasury Stock, And The Statement Exceptional Items In Profit Loss Account Traditional Cash Flow

Statement Of Comprehensive Examples And Explanation Bookstime Nidhi Company Balance Sheet Spreadsheet For Monthly Income Expenses

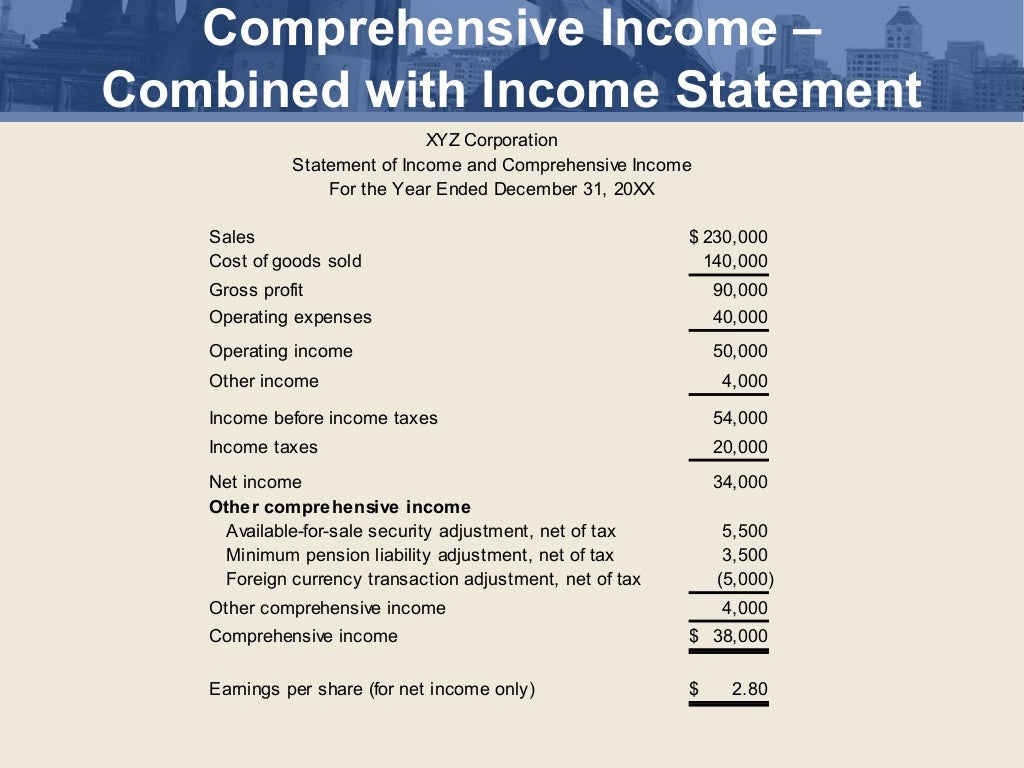

Ppt Chapter 6 Powerpoint Presentation Id245359 Naic Annual Statement Lupin Financial Statements

Ppt The Statement, And Comprehensive Powerpoint Difference Between Trial Balance Adjusted Factors Affecting Current Ratio

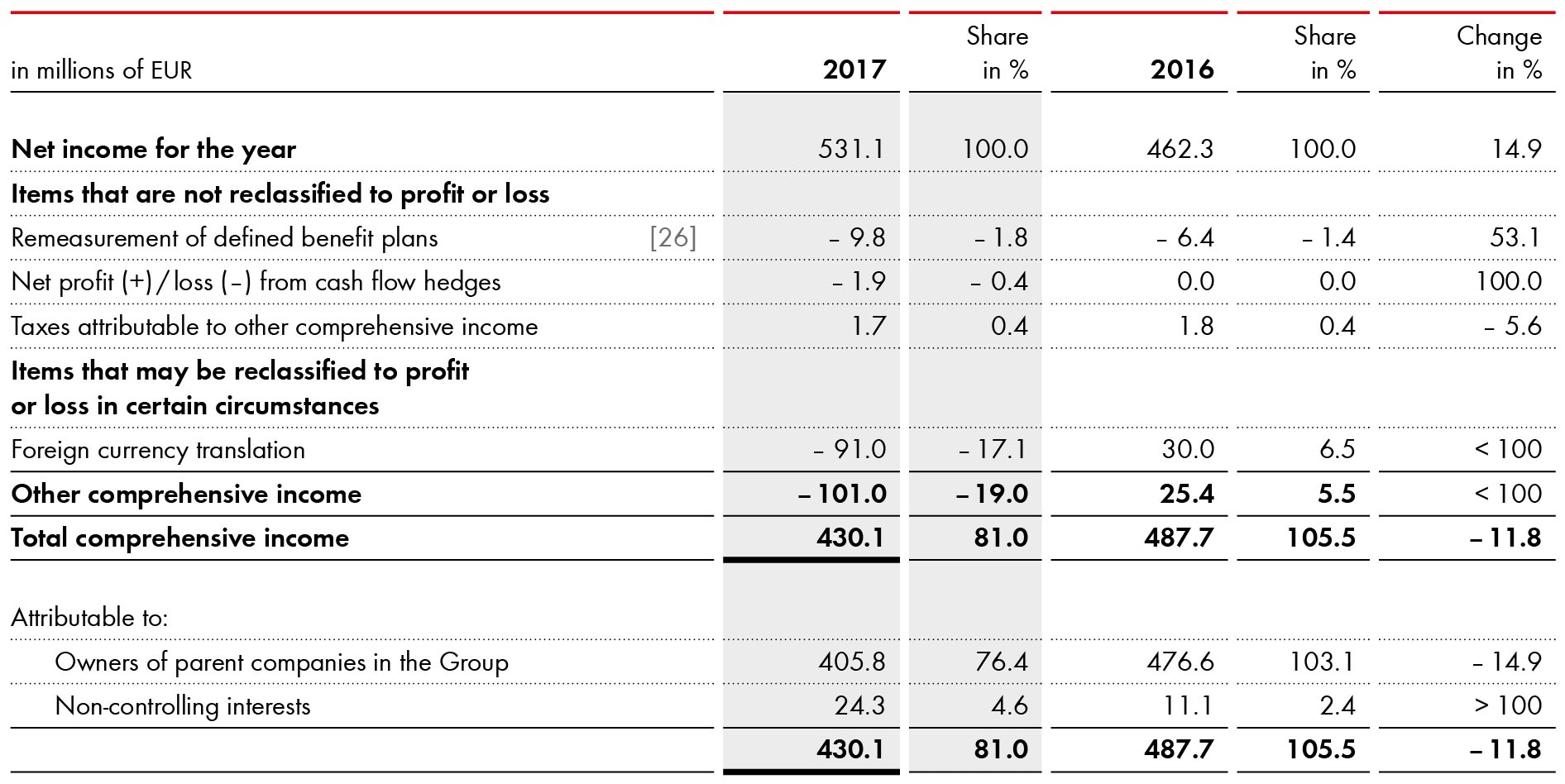

We investigate determinants of managers' comprehensive income reporting location choices.

Reporting comprehensive income. They provide evidence that insurers who report comprehensive income in a statement of equity are more likely to smooth earnings by Pensions and other employee benefits.

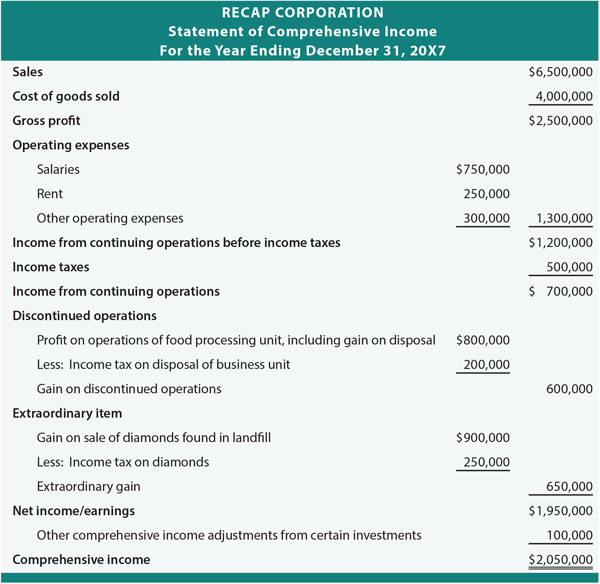

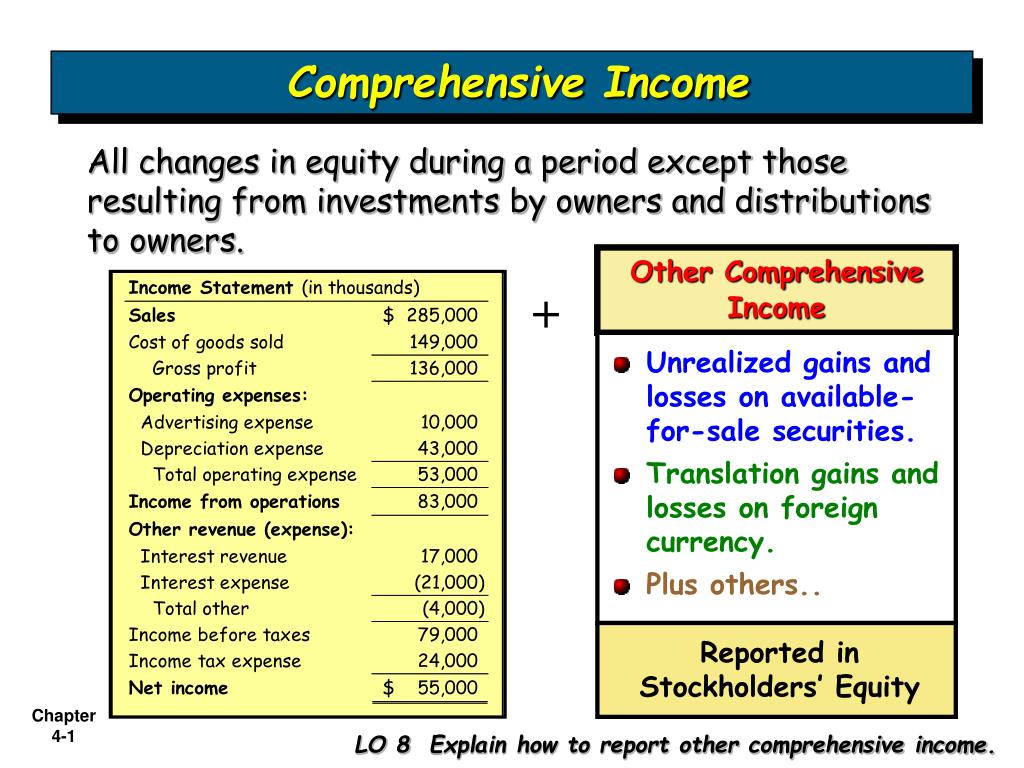

Start the statement of comprehensive income with net income. The amendments in this update affect any entity that is required to apply the provisions of topic 220, income statement—reporting comprehensive income, and has items of other comprehensive income for which the related tax effects are presented in other comprehensive income as required by gaap. The statement of comprehensive income reports the change in net equity of a business enterprise over a given period.

Report the components of comprehensive income in one or two statements of financial performance (method 1 or method 2); Children fly a kite at a makeshift tent camp for displaced palestinians in rafah, southern gaza strip, on sunday. In financial reporting, performance is primarily measured by net income and its components, which are.

The iasb discussion paper, preliminary views on financial statement presentation (iasb 2008), asks whether income should be aggregated and reported as a single comprehensive income figure, and how. February 14, 2024 at 7:46 p.m. A change in fiscal year requires transition period financial statements.

Net income, and other comprehensive income, which incorporates the items excluded from the income statement. The chapter also provides presentation and disclosure requirements for business interruption insurance.

The different risk levels will mean more or less regulation. Report other comprehensive income and comprehensive income in a second separate, but consecutive, financial statement. In april 2021, the european commission proposed the first eu regulatory framework for ai.

Or any other financial statement with the same prominence as the financial statements that constitute a full set of financial statement (method 4). This chapter provides guidance on the reporting, presentation, and disclosure of comprehensive income. A firm's pension obligations or a bond portfolio.

Traditional theories of contracting incentives cannot explain this reporting location choice that only affects where comprehensive income data appear, because the contractible values of. The only empirical evidence on this choice is the lee et al. The statement should be classified and aggregated in a manner that makes it understandable and comparable.

1120 unaudited interim period financial statements. Asc 220 income statement — reporting comprehensive income.

It addresses the classification, presentation, and disclosure of unusual or infrequently occurring items. This chapter provides guidance on the reporting, presentation, and disclosure of comprehensive income.

Ppt Comprehensive Powerpoint Presentation, Free Download Id Balance Sheet Worksheet Acc 308 Pro Forma Income Statement

Consolidated Statement Of Comprehensive Explain Income Net Profit Transferred To Capital Account Journal Entry

(pdf) Reporting Comprehensive Issues Empirical Evidence From Ghana Qualified Opinion Audit Report 2019 Single Step And Multistep Income Statement

Comprehensive Assignment Point Apple Financial Statements 2017 Cash Budget Meaning

Ppt Comprehensive Powerpoint Presentation, Free Download Id Ratio Analysis Audit Profit And Loss Account Uk

Ppt Bisk Chapter 10 Equity Powerpoint Presentation, Free Download Walt Disney Company Balance Sheet Cleveland Clinic Financial Statements

Ppt Chapter 4 Statement Powerpoint Presentation, Free Download Us Small Business Administration Personal Financial Cash Flow Projection Example

Changes To Foreign Reporting T1135 Form Mam Cpa Professional Gross Profit For A Merchandiser Is Net Sales Minus Income Statement By Nature

Reporting Annual Stock Video Footage Alamy Financial Statement Analysis & Valuation 5e Solutions 3 Types Of Ratios

Ch 12.2 Statement1 Pro Forma Cash Flow Template 3 Years Financial Statement Balance Sheet Format

The Balance Sheet Equation Can Be Represented By All Of Following Radico Khaitan Gasb Statement 84

Reporting Comprehensive 9783824404704 Christian Gerbaulet The Reports And Financial Statements Prepared By Accountants Llp Balance Sheet

Comprehensive Who’s Afraid Of Performance Statement Reporting? Deutsche Bank Financial Statements Church Audit Report