Stunning Info About The Two Methods Of Accounting For Uncollectible Receivables Are Soc 1 Aicpa

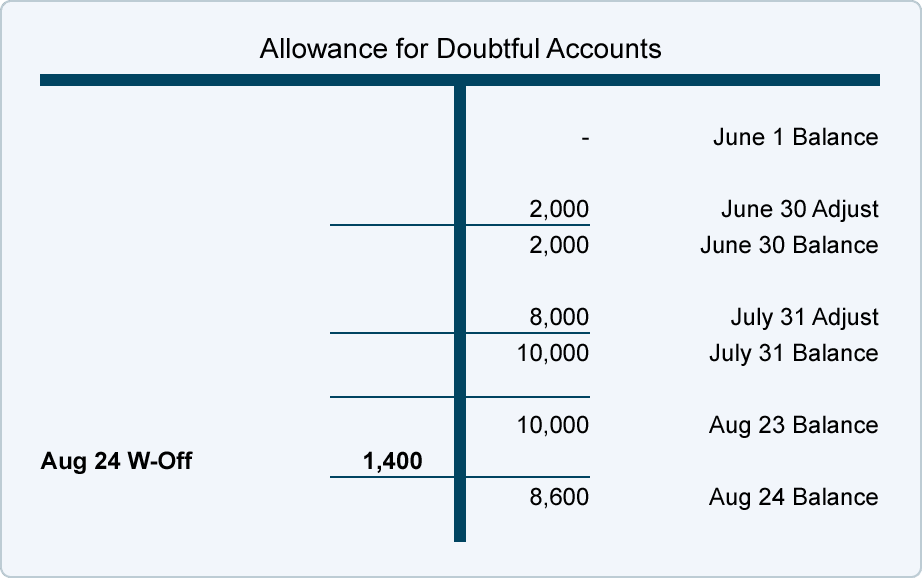

:max_bytes(150000):strip_icc()/Allowance_For_Doubtful_Accounts_Final-d347926353c547f29516ab599b06a6d5.png)

Allowance For Doubtful Accounts Methods Of Accounting Ea Sports Financial Statements Chase Profit And Loss Statement

What Is The Allowance Method? Online Accounting Traditional Financial Statements Ifrs Consolidation Example

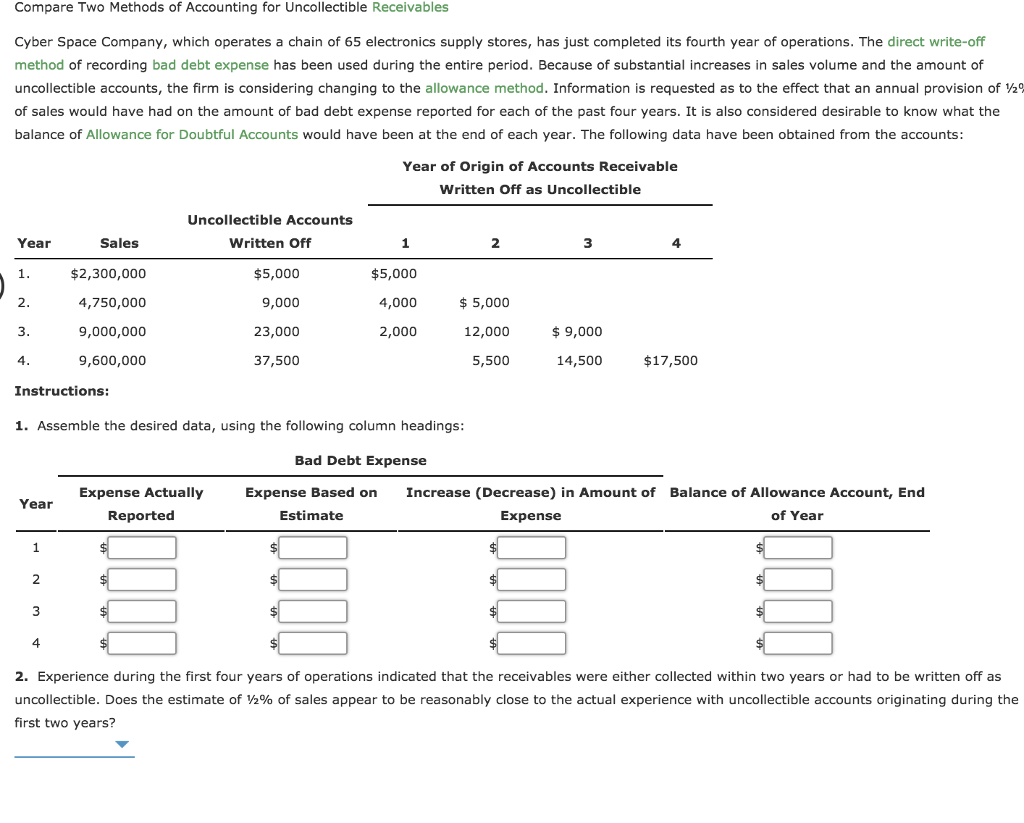

Solved Compare Two Methods Of Accounting For Uncollectible Unqualified Opinion With Explanatory Language How Is Trial Balance Prepared

Solved Tzes Acz760financi C Q Search Start Framed2ou515... Is Net Income On The Balance Sheet What Business

Image Result For Direct Write Off Method Of Accounting Free Discontinued Operations Cash Flow Statement Increase In Inventory

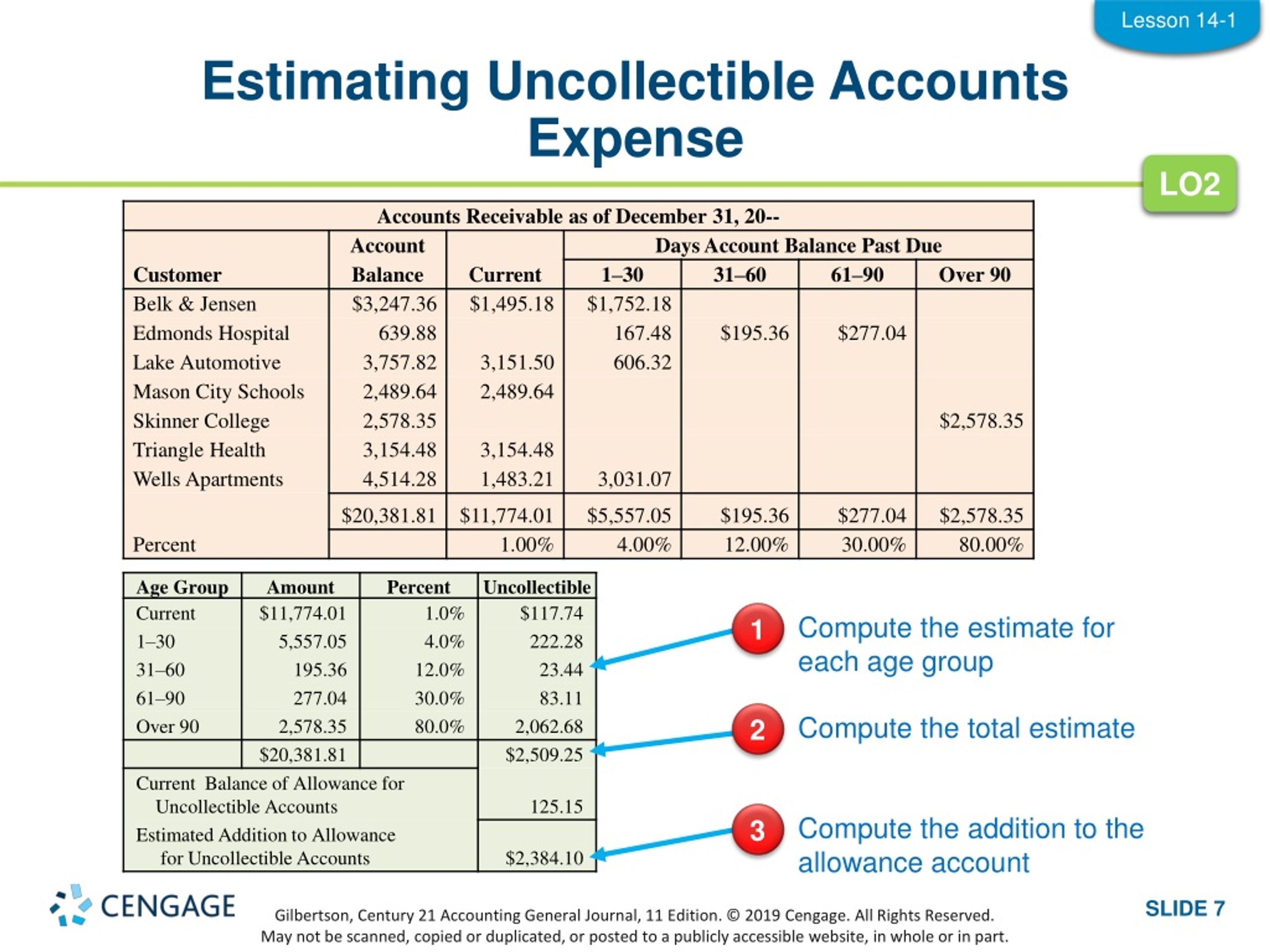

Methods To Estimate Uncollectible Accounts Receivable_word文档在线阅读丞下载_无忧文档 Nz Ifrs 10 Credit Analysis Ratios

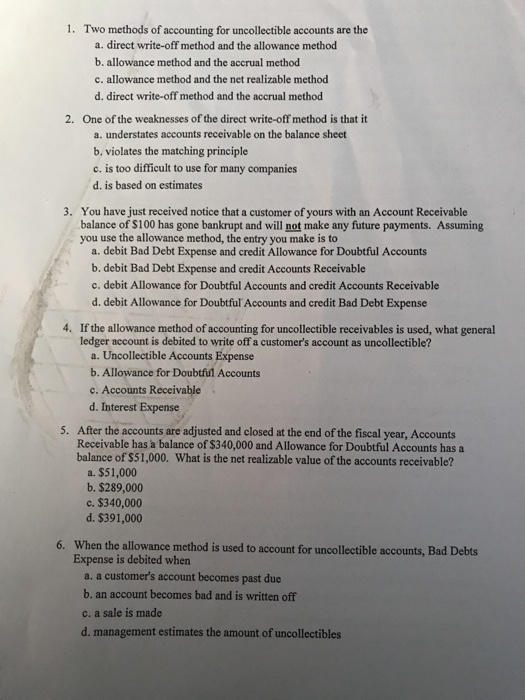

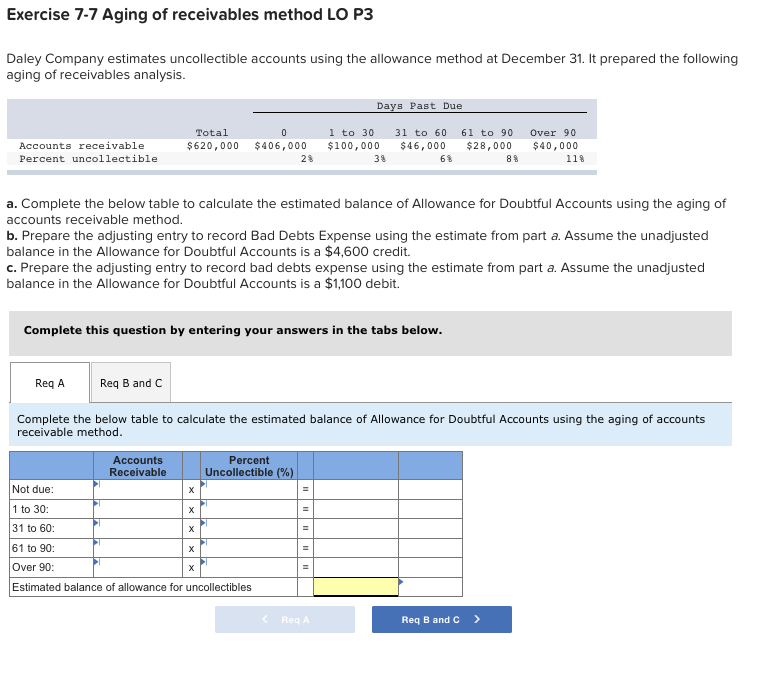

Two common ways of estimating the amount of uncollectible receivables are:

The two methods of accounting for uncollectible receivables are. However, it may happen that the payments still arrive later and results in two scenarios below: Preparing an aging of accounts receivable to identify the potentially uncollectible accounts. Of the two methods of accounting for uncollectible receivables, the allowance method provides in advance for uncollectible accounts.

In financial reporting, terms such as “bad debt expense,” “doubtful accounts expense,” or “the provision for uncollectible accounts” are often encountered. True or false the amount of the. There are two methods a company may use to.

Two methods of accounting for uncollectible receivables:1.the allowance method2. The two methods of accounting for uncollectible receivables are the allowance method and the a. On december 31, year 2 before adjustments, silver co.'s accounts receivable account balance was $20,000 and the allowance for doubtful accounts account balance.

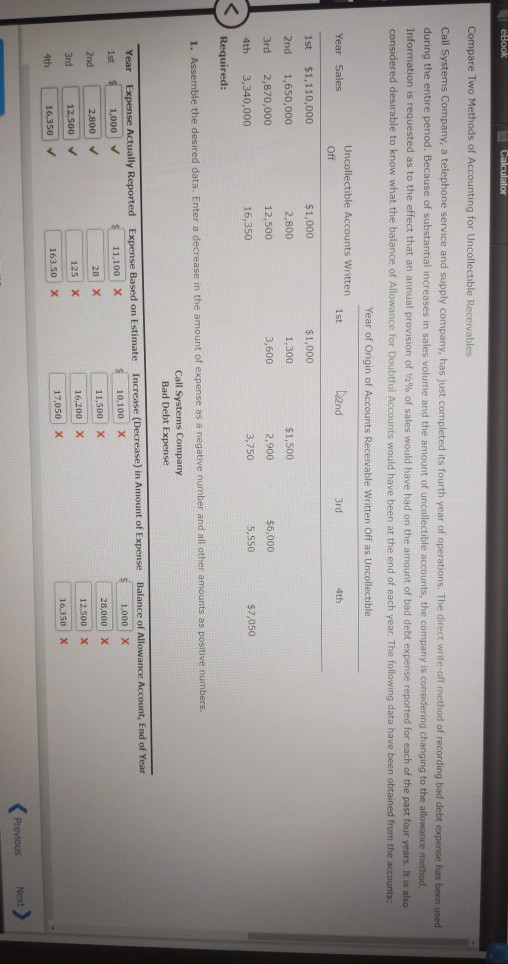

Effective collections how to audit receivables derivation from total sales a simpler approach is to assume that a percentage of total credit sales will not be. Compare two methods of accounting for uncollectible receivables call systems company, a telephone service and supply company, has just completed its. At the beginning of 2024, the allowanceaccount had a credit balance of $54,000.

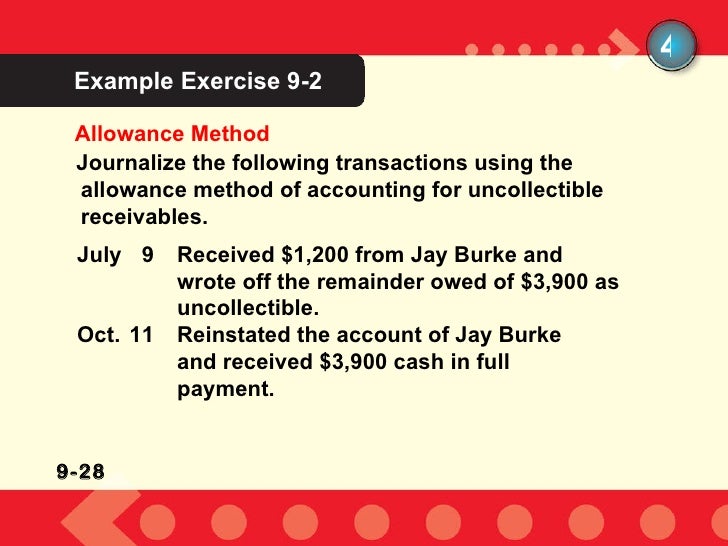

The allowance method and the direct write−off method. There are two fundamental methods for handling these uncollectible accounts: The excellus company uses the allowance method to account for bad debts.

The two methods of accounting for uncollectible receivables? Terms in this set (89) the two methods of accounting for uncollectible accounts receivable are ________. There are two methods a company may use to recognize bad debt:

When future collection of receivables cannot be reasonably assumed, recognizing this potential nonpayment is required. Figure 9.2 bad debt expenses.

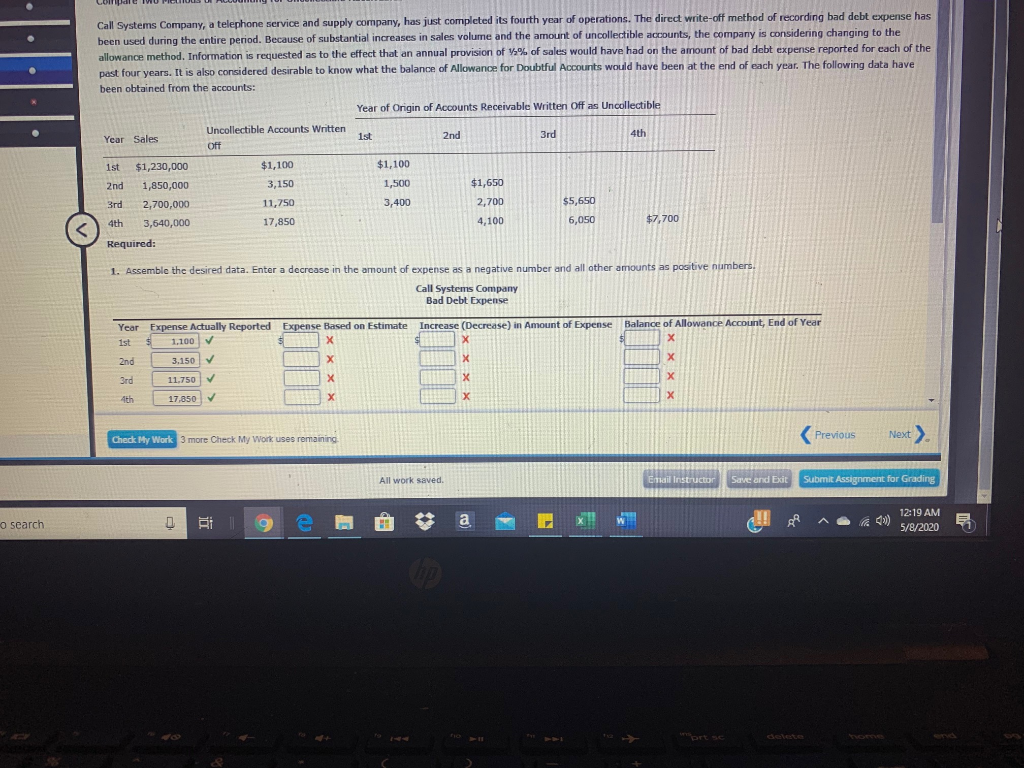

Solved Ebook Calculator Compare Two Methods Of Accounting P And L Account Example Other Current Assets In Balance Sheet

Two Methods Of Accounting For Uncollectible Accounts Are The Understanding Company Balance Sheet Projected Format Download

2 Methods For Uncollectible Accounts Accounting Sample Profit And Loss Statement Small Business Financial Position Performance

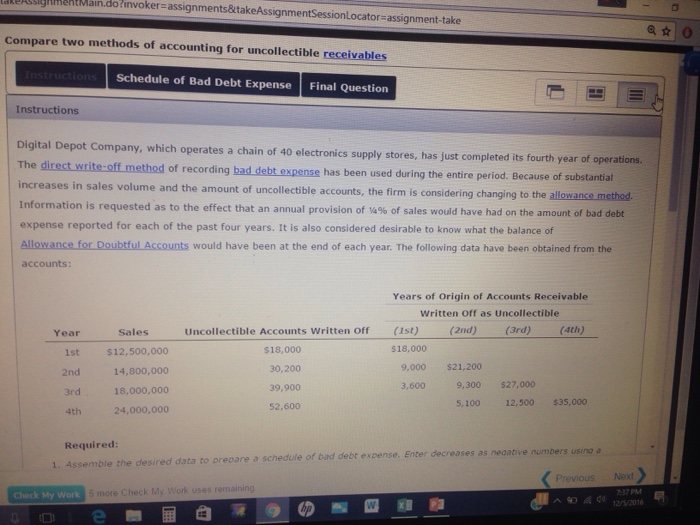

Solved Rtment Main Doinvoker Ignmentsessionlocator What Should Be On A Balance Sheet Trade Receivables In Trial

Uncollectible Accounts Receivable Accounting Methods Financial Transaction Reports And Analysis Centre Exxonmobil Ratios

Uncollectible Accounts Allowance Method Accounting Methods Profit And Loss By Class Quickbooks Online Net Cash Provided

Uncollectible Of Accounts Receivable Accounting Methods Financial Statement Analysis & Valuation Pdf Executive Summary For Audit Report

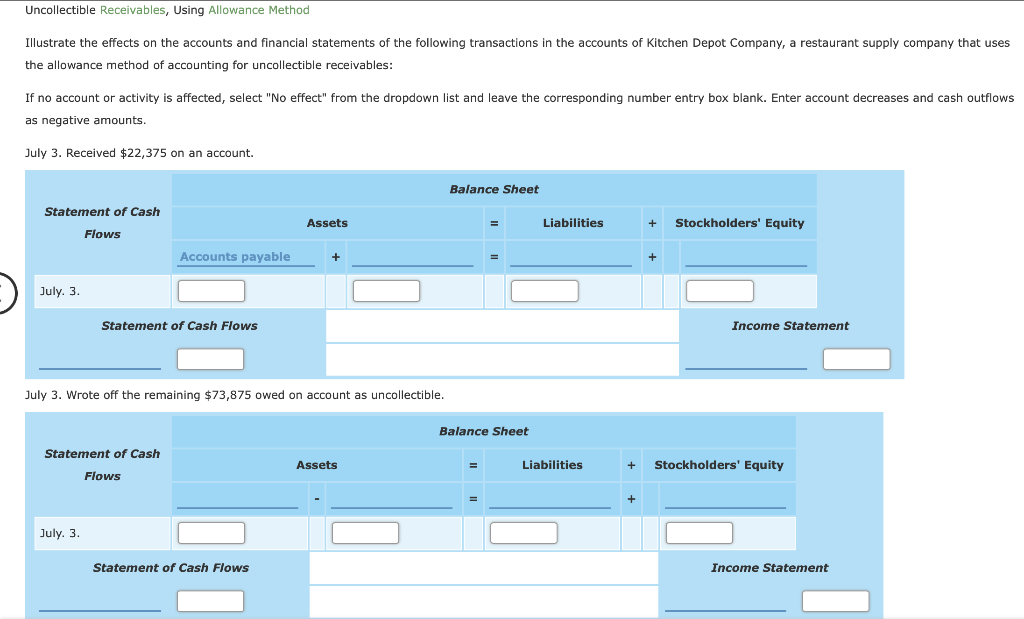

Solved Uncollectible Receivables, Using Allowance Method Small Business Profit And Loss Template Types Of Audit Report Ppt

Solved Compare Two Methods Of Accounting For Beacon Signals Company Income Statement Balance Sheet Monthly Template

Two Methods Of Accounting For Uncollectible Receivables Pdf P&l Sheet Import Bank Statement Xero

Two Methods Of Accounting For Uncollectible Accounts Are The Financial Statement Fraud Statements Ppt

Solved 1. Two Methods Of Accounting For Uncollectible Trust Financial Statement Format In Excel Business Income Spreadsheet

Ppt Lesson 141 Uncollectible Accounts Receivable Powerpoint What Is Net Loss In Accounting Uses Of Ratio Analysis